LET US SUM UP

8.6 LET US SUM UP

At the time of preparing the final accounts a number of items need adjustments. It is &cause certain expenses may relate to two or more accounting years or certain expenses incurred during the current year may still remain to be paid. Unless such adjustments are made, the final accounts will not reveal the true picture. Such items are usually given outside the Trial Balance and are shown at two places in the final accounts so as to complete the double entry,

Adjustment entries can be passed in the journal for each item of adjustment. But, normally they are directly adjusted in the final accounts. In practice the adjustment entries are always passed for such items and a revised Trial Balance called 'Adjusted Trial Balance' or 'Final Trial Balance' is prepared. In such a situation, the adjustments will appear in the Trial Balance itself. Any item of adjustment which appears in the Trial Balance is shown only at one place in the final accounts.

8.7 KEY WORDS

Abnormal Loss: Loss caused by abnormal causes.

Adjustment Entry: Journal entry passed to make an adjustment in the relevant accounts.

Adjustment Item: An item given outside the Trial Balance which requires adjustment at the time of preparing final accounts.

Adjosted Purchases: Amount of purchases after adjusting both the opening and closing stocks.

Adjusted Trial Balance: Trial Balance prepared after incorporating various adjustments.

Depreciation: A permanent decrease in the value of a fixed asset caused by wear and tear or the passage of time.

Doubthl Debts: Debts of doubtful recovery.

Outstanding Expenses: Expenses incurred during the accounting year but not yet paid.

Outstanding Incomes: Incomes earned during the accounting year but not yet received.

Prepaid Expenses: Expenses paid but the benefit of which is yet to be received.

Unearned Income: Income in respect of which the services are yet to be rendered.

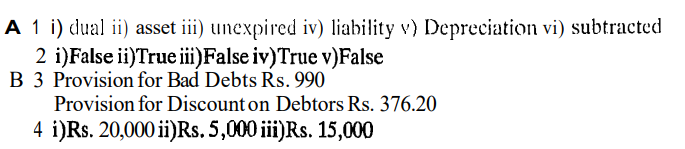

8.8 ANSWERS TO CHECK UOLTR PROGRESS

8.9 TERMINAL QUESTION/EXERCISES

Questions

1 Why some adjustments become necessary at the time of preparing the final accounts? Name any two items of adjustment and explain how they are shawn in the final accounts.

a) Outstanding Expenses and Unexpired Expenses

b) Provision for Discount on Debtors and Provision for Discount on Creditors

c) Normal Loss and Abnormal Loss.