Saturday, September 30, 2023

LET US SUM UP

3.6 LET US SUM UP

When the number of transactions in a business are too large, it becomes difficult to record all

of them in the Journal. Hence, it is sub-divided into a number of special journals called

subsidiary books. Each subsidiary book is used foi. recording only one category of

transactions. The subsidiary books generally used are: (i) Cash Book, (ii) Purchases Journal,

(iii) Purchases Returns Journal, (iv) Sales Journal, (v) Sales Returns Journal, (vi) Bills

Receivable Journal, (vii) Bills Payable Journal, and (viii) Journal Proper

All cash trans:u:tions are recorded in Cash Book. There are three types of cash books. They

are: (i) Simple Cash Book, (ii) Two Column Cash Book, and (iii) Three Column Cash Book.

Simple Cash Book has only one amount column on both sides. All cash receipts are

recorded on the debit side and all cash payments on the credit side. It serves the purpose of

Cash Account. The Two Column Cash Book has an additional column for cash discount on

both sides. he discount allowed is recorded on the debit side and the discount received on

the credit side. The Three Column Cash Book provides one more column on both sides for

recording the banking transactions. All deposits into the bank are recorded in the bank

column on the debit side of the cash book and all withdrawals on the credit side. This serves

the purpose of a Bank Account.

When cash book and the pass book are compared, it is often found that the balances shown

by these two books differ. There may be many causes leading to difference. A Bank

Reconciliation Statement is prepared to explain the causes of difference and take the

necessary follow up action. It can be prepared either by taking cash book balance as the

starting point or by taking pass book balance as the starting point, It can also be prepared by

taking the adjusted balance of the cash book as the starting point. The adjusted balance of

the cash book is arrived at by passing corresponding entries in the cash book for items which

' appeared in the pass book only.

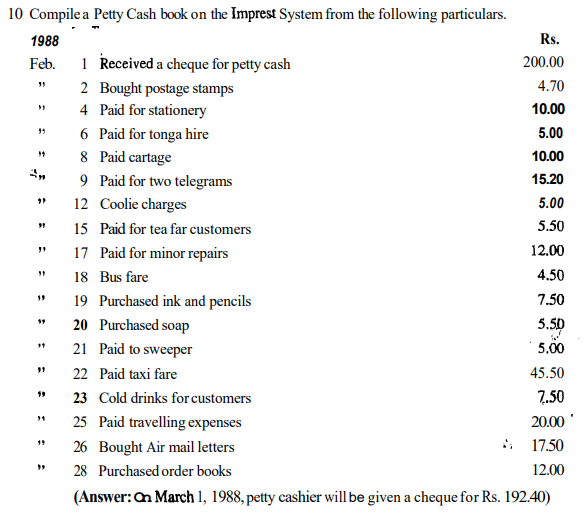

A Petty Cash Book can also be prepared for recording payments of various petty expenses.

It is maintained on imprest system which means advancing a fixed amount to the petty

cashier. The maintenance of Petty Cash Book saves a lot of labour and time.

3.7 KEY WORDS

Bank: An organisation which deals in money by accepting deposits and lending money to

those who need it. It also provides various other services to its customers.

Bank Charges: Amou~lt charged by bank for providing various services to its customers.

Bank Reconciliation Statement: A statement reconciling the bank balance as shown by the

cash book with that of the pass book by showing all causes of difference between the two.

Cheque: An instrument used for withdrawing money from the bank. It is an unconditional

order on the bank made by its customer, instructing the bank to pay the amount specified

therein to the person named in the cheque or to his order.

Contra Entry: When both the debit and the credit aspects of a transaction are recorded in

the cash book itself, it is called a contra entry.

Dishonour: Refusal by bank to make payment against the cheque.

Endorsement: A written statement made and signed by the payee at the back of the cheque

for its transfer.

Favourable Balance: Balance indicating that the customer has got money in his account

with the bank.

Imprest System: A system of advancing a fixed amount to the petty cashier.

Pass Book: A book supplied by the bank to its customers showing his transactions with the

bank.

Standing Instructions: Instructions to the bank for making certain payments and

collections regularly on behalf of the customer

Subsidiary Book: A special journal used for recording a particular category of transactions.

3.9 ANSWERS TO CHECK YOUR PROGRESS

A 2 (a) iii (b) i (c) iii (d) ii (e) iii

3 (i) Cash (ii) credit (iii) debit (iv) credit (v) overdraft (vi) contra entry

(vii) credit (viii) cash

,B 4 (a) ii (b) i (c) ii (d) i (e)'ii (f) i (g) i (h) ii

5 The cash book of a trader showed a bank balance,of Rs. 7,500 on December 31,1987.

On going through the cash book it was found that: (i) two cheques for Rs. 500 and Rs. 700 deposited on December 28 were credited in the pass book on January 4, 1988;

(ii) Three che4ues for Rs. 500, Rs. 900 and Rs. 1600 issued on December 29, 1987 were

presented to tlie bank for payment on January 7, 1988; (iii) Bank had credited the trader

for Rs. 125 as interest and had debited him for Rs. 10 as bank charges for which there

were no corresponding entries in the cash book.

Prepare a Bank Reconciliation Statement as on December 31, 1987.

(Answer: Balance as per Pass Book Rs. 9,015)

6 Prepare a Bank Reconciliation Statement on December 31, 1987 from the following

particulars.

Ks

1 Overdraft as per cash book 10,210

2 Interest and bank charges appeared in pass book only 305

3 A cheque debited in cash book but not credited by bank 300

4 Cheques issued but not cashed by customers up to Deceniber 3 1, 1987 2,320

5 Cheques paid into bank but not yet cleared 1,550

6 A Bill Receivable discounted with the bank on November, 1987,

dishonoured on December 30, 1987. No entry was made in the

cash book. 800

(Answer: Overdraft as per Pass Book Rs. 10,845)

7 When Madhav & Co. Ltd, received its bank statement for the period ending on June 30,

1987, the balance therein did not agree with tlie balance as per cash book. The Bank

statement showed a balance of Rs. 12,000. The following discrepancies were noticed,

1 A cheque for Rs. 400 paid on June 30 was not credited by the bank until July 2,

2 Bank charges amounting to Rs. 20 were not entered in the cash book.

3 A debit of Rs. 70 appeared in the cash book in respect of a cheque which had been

retunied by the bank marked 'out of date'. The cheque was revalidated by the

customer and received by Madhav Q Co. Ltd. in July. It was deposited into the

bank again on July 6.

4 A standing instructioii for payment of annual subscription amounting to Rs. 40 was

not entered in the cash book.

5 On June 26, the Managing Director gave the cashier a chequc for Rs. 800 to pay into

his petsonal account at the bank. The cashier paid it into the company's account by

mistake.

6 On June 29, two customers paid Rs. 700 and Rs. 800 directly into the cotlipany's

bank account. The concerned advices had not been received by the company until

July 3.

7 Rs. 250 paid into the bank was entered twice in the cash book.

8 Cheques amounting to Rs. 3,500 were issued but not yet presented for payment.

9 A customer of the company who received a cash discount of 1.5% on his acco&t of

Rs. 1,000 paid the company by cheque on June

10. The cashier by mistake entered

,, the gross amount in the bank column of the cash hook.

Prepare the Bank Reconciliation Statement.

(Answer: Balance as per Cash Book Rs. 6,995)

8 On June 26,1988, I had an overdraft of Rs. 7,500 as shown by my pass book. Cheques

amounting to Rs. 1,000 had been paidhto the bank on June 24, but of these only Rs,

750 was credited in the pass book. I had also issued cheques amounting to Rs. 2,500 of

,which Rs. 2,000 worth only have been presented. There is a debit in my pass book of

, Rs. 75 for interest. I also find that a cheque for Rs.,60 which I had debited to Bank

* Account in my pass books has been omitted to be banked. An entry of Rs. 300 of a

i payment by a customer direct into the bank appears in the pass book only.

Prepare a Reconciliation Statement as on June 30, 1988.

(Answer: Overdraft as per Cash Book Rs. 7,915)

9 Prepare a Bank Reconciliation Statement from the following particulars and find out

the balance as per pass book on December 3 1,1987. The bank balance as per cash

book was Rs. 5,600.

1 Cheques Received from the foIlowing persons were paid into the bank in

December 1987 but were credited by the bank in January 1988.

Shekhar Rs. 2,500

Madan Rs. 3,200

Rakesh Rs. 4,480

2 Cheques issued by the firm in December 1987, were cashed in January 1988.

Ahmed Rs. 700 I

David Rs. 900

Siva Rs. 550

3 The pass book showed a credit of Rs. 100 for interest.

4 'A debit of Rs. 20 for bank charges appeared twice in the pass book. However, it

did not appear in cash book at aI1.

5 Jagdeep, a customer, deposited a cheque of Rs. 100 directly into f rm's bank

account for which there was no entry in the cash book.

6 A cheque for Rs. 100 received from Pradeep and deposited into the bank was

- returned dishonoured.

7 A cheque received from Anil for Rs. 690 was entered twice in the cash book.

(Answer: Overdraft as per Pass Book Rs. 3,060)