3.4 BANK 'RECONCILIATION STATEMENT

You learnt that the firm records all trans&tions relating to its bank account 'in a Three

Column Cash Book. All deposits into the bank are recorded on the debit side of the cash book and all withdrawals from the bank on the credit side. The bank also maintains the

firm's account in its books. It credits customer's account with all deposits made by him and

' debits his account with all withdrawals made by hirn. The bank provides a copy of this

accou~lr to the customer in the form of a bank statement or a pass book. The proforma of

such a statement or the pass book is given in Figure 3.2.

When the busiliessinari receives the bank statement or the pass book from the bank, Ile

cornpares it with the cash book. Noimally, entries in the cash book would tslly with those in

the pass book and the balarices shown by both the books should also be the same. But in

practice, they generally differ. This happens if there are some en~ries which have been

recorded in the cash book but they do not appear ir! the pass book. Similarly, there may be

some entries which have been recorded in the pass book but they do not appear in the cash

book. The difference can also arise on accouiit of errors co~nmitted either by tlie film or by

thc bank in the lecording of various transactions, Let us therefore understand clearly the

exact causes of differences in tlle balances of these two books befo1-c we recor~cile the

balances of these two books.

3.4.1. Causes of Difference

The main causcs that lead to disagreerne:~t in the balances of the cash book and the pass

book are as follows :

1- Cheques issucd but not yet presented for payment:

The passage you've provided describes the common time lag between the recording of check transactions in a business's cash book and when the bank actually debits the company's account. This time lag can result in discrepancies between the cash book balance and the balance shown in the bank's passbook (or statement) for the business. Here's a breakdown of the scenario described:

Recording in Cash Book: When a business makes a payment by issuing a check, it records the transaction in its cash book immediately. In this case, the business wrote a check for Rs. 3,000 on December 28, 1987, to pay a creditor. So, in the cash book, this payment is recorded on December 28, 1987.

Bank's Debit: However, the bank will only debit the business's account when the payee (the creditor in this case) presents the check for payment. In this example, the check was presented to the bank for payment on January 2, 1988. As a result, the bank records the debit to the business's account on January 2, 1988.

Passbook Balance: When the business receives its passbook statement, which is typically sent by the bank at regular intervals (e.g., monthly), the balance shown in the passbook will reflect the bank's records. In this case, since the bank recorded the debit on January 2, 1988, the passbook will show a lower balance by Rs. 3,000 compared to the cash book on December 31, 1987.

Discrepancy: This time lag between the cash book and the bank's recording can lead to a temporary difference in the balances. In this case, the passbook balance is higher by Rs. 3,000 because the bank hasn't yet accounted for the check issued by the business on December 28, 1987, as of the passbook's reporting date.

Reconciliation: To reconcile these discrepancies, businesses typically perform a bank reconciliation. This process involves comparing the cash book transactions with the bank statement, taking into account items like outstanding checks (checks issued but not yet presented) and deposits in transit (deposits made but not yet cleared by the bank). The goal is to ensure that both the cash book and the bank statement balance match after considering these timing differences.

2 - Cheques deposited into the b:ink hut bok ye1 coilected:

The passage you've provided explains the accounting treatment for checks that have been deposited into a company's bank account but have not yet been collected by the bank. This process can lead to differences between the cash book balance and the balance shown in the bank's passbook or statement. Here's a breakdown of the scenario described:

Recording in Cash Book: When a company receives a payment by check, it sends the check to the bank for collection and immediately records the transaction in its cash book on the "receipts" side. This recording increases the bank balance as per the cash book.

Bank's Credit Delay: Even though the company records the check in its cash book, the bank will not credit the company's account until the check is actually collected. This means that the bank's balance, as shown in the passbook, remains unaffected until the check is collected and credited by the bank.

Passbook Balance: When the company receives its passbook statement, it reflects the bank's records. In this case, the passbook balance will not include the credit for the check until it is collected by the bank. Therefore, the passbook balance may be lower than the cash book balance as of the passbook's reporting date.

Collection Date Matters: The timing of when the check is collected by the bank is crucial. In your example, if the firm sends a check of Rs. 2,000 on June 28 for collection, but it's not collected by the bank until July 6, the passbook balance as of June 30 will not include this credit. Therefore, the cash book balance and the passbook balance will be different as of that date.

Reconciliation: To reconcile these discrepancies between the cash book and the passbook, companies typically perform a bank reconciliation. This process considers outstanding checks (checks sent for collection but not yet credited) and other timing differences to ensure that both balances match.

3 - Bank charge

Bank charges refer to fees or costs that banks impose on their customers for various services and transactions. These charges are a way for banks to generate revenue and cover the costs associated with providing banking services. The specific types and amounts of bank charges can vary from one financial institution to another and may also depend on the type of account and the services used by the customer. Common examples of bank charges include:

Monthly Maintenance Fees: Many banks charge a monthly fee for maintaining a checking or savings account. However, some accounts may waive this fee if certain conditions are met, such as maintaining a minimum balance or receiving a certain amount of direct deposits.

ATM Fees: Banks often charge fees for using ATMs that belong to other banks or are located outside their network. Additionally, there may be fees imposed by the ATM owner itself.

Overdraft Fees: If you spend more money than you have available in your account, the bank may charge you an overdraft fee for covering the shortfall. Some banks also offer overdraft protection programs for a fee.

Wire Transfer Fees: Banks typically charge fees for sending or receiving wire transfers, whether they are domestic or international. The fees can vary widely depending on the destination and currency.

Transaction Fees: Certain types of transactions, such as cashier's checks, money orders, and stop payment requests, may come with associated fees.

Foreign Transaction Fees: When you use your debit or credit card for purchases in foreign currencies or when abroad, you may incur foreign transaction fees, which are typically a percentage of the transaction amount.

Account Closing Fees: Some banks may charge a fee when you close your account, especially if it's done shortly after opening.

Paper Statement Fees: Many banks encourage customers to go paperless by offering electronic statements for free, but they may charge a fee for mailing paper statements.

Insufficient Funds (NSF) Fees: If you attempt to make a payment or write a check with insufficient funds in your account, the bank may charge you an NSF fee, also known as a returned item fee.

Safe Deposit Box Rental: Banks offer safe deposit boxes for storing valuable items, and they typically charge an annual rental fee for this service.

Account Research Fees: If you request detailed account statements or research assistance from the bank, they may charge a fee for these services.

It's important for account holders to carefully review their bank's fee schedule and terms and conditions to understand what charges they may incur. Additionally, some banks may offer fee waivers or discounts to customers who meet specific criteria, such as maintaining a high account balance or using certain banking services. To minimize bank charges, consumers should choose accounts and services that align with their financial needs and habits and be mindful of their account balances and transactions.

4 - Interest allowed by the bank :

The banks normally do nqt allow any interest on the

cunant account balances. But if such interest is allowed, the bank credits it to the customer's

account. This increases the balance in the pass book. The finn would pass the corresfionding

entry in the cash book only when it receives the intimation from the bank or when it notices

it in the pass book. Hence, the cash book balance will be lower till such entry is made.

5 - Interest on overdraft:

When the bu'iinessman requires more funds he may request the

bank for overdraft facility which means pemlitting hi~n to draw nnore than the amount

av.aiIable in his account. When the businessman actually withdraws more than the available

amount, he is said to have utilised the overdraft facility. The bank charges interest on the

amount overdrawn and debits the same to his account periodically. The firm records the

corresponding entry for interest on overdraft only when the pass book is received. Hence,

the balance in the two books would differ till the entry is passed in the cash book.

6 - Amount collected by bank on standing Enstrmclions:

The businessman often issues

standing instructions authorisiilg his banker to collect on his behalf certain amounts due to

him such as interest, dividends, etc. The bmk credits the customer's account as and when it

collects such amounts and sends the necessary intimation to him. The firm will pass'the

corresponding entry in the cash book when it receives such intimation or when it notices it

in the pass book. Thus, as' on the date of reconciliation, the balance as per cash book may be

lower than the b'alance as per pass book.

7 - Payment made by the bank as per the standing instructions: '

The businessman may

also issue standing instructions to his banker to make certain payments on his behalf such as

insurance premium, rent, etc. When the banker makes such payments, he would immediately

debit the customer's account. So, the balance in thc pass book would get reduced. If the

corresponding entries for such payments have not been recorded in the cash book, the

ba1aice.a~ per cash book would remain unchanged.

8 - Direct payments into the bank made by firm's customers:

Sometimes, a customer may

directly deposit an amount into the firm's account. The firm shall record it in the cash book

only when it learns about such deposit. But, {he pass book would show the entry on the date

of deposit itself. If, by the date of reconciliation, such entry has not been passed in the cash

book, the balance shown by pass book will be higher than the balance as per cash book.

9 - Dishonbur of cheques or bills:

As already stated whencheques are sent to the bank for

coll~ction they are entered in the ysh book immediately. But no entry appears in the pass

book till they are collected by the bank. Soinetimes, for one reason or the other, the cheques

are dishonoured. In th2 case the bank will not make any entry in its books and returns such

cheques to the firm. The same thing applies to the bills receivable sent for collection to the

bank. On receiving the dishonoured cheques or bills the firm has to pass a reverse entry in

the cash book. But, till such entry is passed the balances shown by the cash book and the

pass book bould differ.

10 Errors:

It is quite possible that while recording the transactions in the cash book some

errors Might have been committed by the firm. For example, a cheque deposited in the bank

may not be recorded at all, oi is recorded on the wrong side in the cash book. Similarly, the

bank may also commit some errors while recording entries in the customer's account. For

example, a cheque collected on behalf of a customer is entered in some other account. Such

errors would also lead to the disagreement of the balances in the cash book and the pass

book.

3.4.2 What is Bank Reconciliation Statement?

By comparing the entries in the cash book with those in the pass book you can easily '

ascertain the exact causes of difference 6etween the balance as per cash book and the

balance as per pass book. In order to reconcile these balances every firm prepares a

statement showing all the causes of differences. This statement is called Bank Reconciliation

Statemefit-and is pepared periodically. The main objective of preparing such a statement is

to account for the difference between the cash book and the pass book balances and pass the

ne'cessary correcting entries in the books of the firm.

Thus, Bank Reconciliation Statement canL

be defined as a statement which reconciles

the balance as per cash book and the balance as per pass book showing all causes of

' difference between the two.

3.4.3 Preparation-of Bank Reconciliation Statement

The Bank Reconciliation Statement is prepared at the end of a quarter, half year or a year as

the firm may consider desirable and convenient. It can be prepared in two ways :

i) Take the balance as per cash book as the starting point, adjust the effect of each item

causing the difference, and arrive at the balance as per pass book.

ii) Take the balance as per pass book as the starting point, adjust the effect of each item

causing the difference, and arrive at the balance as per cash book.

Whatever be the method, first of all you must analyse the effect of each item on the balance

of the book which you are using as the starting point. In other words, whether it has led to a

higher balance or a lower balance in that book. This helps you to decide whether a

particular item is to be added to, or subtracted from, such a balance.

Suppose, you start with cash book balance as the base and the item causing the difference is

the bank charges of Rs. 100. This item appears in the pass book but not in the cash book.

The bank charges would appear in the withdrawals column of the pass book which means

that the pass book balance had decreased by Rs. 100. Since it has not been shown in the

cash book, the cash book balance remained unaffected, it did not decrease. Hence the cash

book balance would be higher than the pass book balance by Rs. 100. If we now subtract this

amount from the cash book balance it will reconcile with the pass book balance. Take

another example. The bank collected Rs. 500 as interest on securities on behalf of the firm.

But, the same had not been recorded in the cash book. This item would appear in the deposit

column of the pass book which means the pass book balance had increased by Rs. 500.

Since it had not been shown in the cash book, the cash book balance remained unaffected, it

did not increase. Hence, the cash book balance would be lower than the pass book balance

by Rs. 500. If we now add this amount to the cash book balance it will reconcile with the

pass book balance.

If you were to start with pass book balance as the base you would do just the reverse of

what you did when you started with cash book balance as the base. You will add Rs. 100

relating to the item of bank charges because it leads to a lower balance in the pass book and

subtract Rs. 500 relating to interest on securities collected by the bank because it had

increased the pass book balances.

Generally, the firms adopt the first method because the Bank Reconciliation Statement is

prepared primarily for the verification of the bank balaqce as shown by the cash book.

From the above examples it should be clear to you that in case you start with cash book

balance you should add all those items which have been responsible for lower balance in the

cash book and subtract those which have been resporisible for a higher balance. Let us, for

convenience, list the items which would generally be added and subtracted when cash

balance is used as the starting point

To be added

1 Cheyues issued but not yet presented

2 Interest allowed by the bank

3 Interest and dividends collected but not recorded in the cash book

4 Direct deposits by customers in the firm's bank account.

To be subtracted

1 Cheques deposited but not yet collected

2 Bank charges

3 Interest on overdraft

4 Amounts paid by the bank under standing instructions but not recorded in the cash book

5 Cheques dishonoured but no entry made in the cash book for the dishonour

If the pass book balance is taken as the starting point, just reverse the above process. Add

those which are to be subtracted from the cash book balance as per the above list and

subtract those which are to be added to the cash book balance as per the above list.

The above analysis wit1 help you to prepare the Bank Reconciliation Statement correctly.

Look at Illustration 4 and study how a Bank Reconciliation Statement is prepared with cash

book balance as the starting point.

Illustration 4

From the following particulars, prepare a Bank Reconciliation Statement as on December

31, 1987:

On December 31, 1987 Mohan's cash book showed a debit balance of Rs. 7,800. The

balance as per pass book was Rs. 10,300. On comparing the cash book with the pass book,

the following discrepancies were found :

1 Two cheques for Rs. 1,600 and Rs. 2,000 iisued on December 23 have not been

presented to the bank for payment.

2 A cheque for Rs. 1,200 was deposited in the bank on December 29, but it was credited

by the bank on January 5,1988.

3 There was a credit entry in the pass book for Rs. 520 in respect of dividend received by.:!

the bank on behalf of Mohan. This had not been recorded in the cash book.

4 Rs. 300 was deposited by a customer directly into the bank.

5 The bank charged Rs. 60 as their commission for collecting an outstanding cheque. no'

entry for this appeared.in the cash book.

6 A cheque for Rs. 500 received from Gopi and deposited in the bank was dishonour but no entry was recorded in the cnsh book for the dishonour.

7 A cheque for Rs. 160 was entered in the cash book but it was not sent to the bank for collection.

Note:

The statement bears a heading 'Bank Reconciliation Statement' and mentions the datetor Ghibh' If' ' ''

reconciliation is done. So, whenever you prepnre a Bank Reconciliation Statment make sure thnt it bears

this heading along with the date of reconciliation.

The Bank Reconciliation Statement can also be prepared by 'plus and minus method .'In . that case you will have two separate amount columns, one for additions and the other for

subtractions. The first column is called 'plus column' and the secend column is called minus column. The Bank Reconciliation Statement prepared acooding td this methud will '

appear as follows:

Now, look at Illustration 5 and study how a Bank Reconciliation Statement will be prepared

with pass book balance as the starting point.

Illustration 5

From the following, prepare a Bank Reconciliation Statement of Radhey La1 as on March

3 1,1988. Balance as per pass book as on March 3 1,1988 was Rs. 22,000.

1 Cheques amounting to Rs. 9,000 were deposited in the bank during March, but credit

was given only for Rs. 7,000.

2 The bank paid insurance premium of Rs. 300 on March 20, but it was not entered in the

cash book.

3 A discounted bill receivable for Rs.1,500 was returned dishonoured to the bank on

March 27, but the corresponding entry in the cash book was made in April.

4 A cheque for Rs, 800 received on March 29 was entered in the cash book, but it was

sent to the bank on April 3.

5 Of the cheques amounting to Rs. 3,000,issued to creditors, the cheques for Rs. 1,800

only were presented for payment.

6 The bank charges debited in the pass book amouiited to Rs, 50.

7 Interest on securities collected a@ credited by the bank amounting to Rs. 1,000 was not

entered in the cash book.

3.4.4 When there is an Overdraft ?

You know when a businessman withdraws from the bank more money than is available in

his account, it is said that he has an overdraft (an unfavourable balance) in his bank account.

It is one of the most commonly used nletllod of borrowing money from the bank.

You have leasnt the method of preparing a Bank Reconciliation Statement when the firm has

a favourable balance in the bank. Let us now study how Bank Reconciliation Statement will

be prepared when the firm has an unfavourable balance (an overdraft).

You know when the firm has a favourable balance the cash book shows a debit balitnce. But

when the firm has an overdraft, it will show a credit balance because, in such a situation, the

bank is a creditor for the firm. As for the pass book, when the firm has favourable balance it

shows a credit balance and when the firm has an overdraft it will show a debit balance,

because for the bank the firm is n debtor when there is an overdraft. In other words it can

be stated that when cash book shows a credit balance or, when pass book shows a debit

balance, the firm has an overdraft.

The prepaiation of the Rank Reconciliation Statement does not differ much whether there is

a favourable balance or an overdraft, specially if you follow the 'plus and minus method'.

You know when the firm has a favourable ba!snce, it is shown in plus column of the Bank

Reconciliation Statement. But, if there is an overdraft it will be sliown in the minus column.

This is the main point you have to remember while preparing a Bank Reconciliation

Statement when there is an overdraft. The treatment with regard to items causing difference

between the balances of the two books remains the same.

If, however, you do not follow the plus and minus method you will have to analyse first the

effect\of each discrepancy on the overdraft and then decide whether the amount involved is

,to be added or subtracted. When you make such analysis you will observe that the effect of

each discrepancy on overdraft will be just the reverse of what it would be on a favourable

I balance. For example, if bank chargcs are found to be unrecorded in the cash book which

shows a favourable balance, this onlission is considered responsible for a higher balance in

the cash book and so, while preparing Bank Reconciliation, it is subtracted from the balance.

But in case of an ovcnlrnft orr~itting to record the bank charges would mean a lower amount

of overdraft in the cash book and so, while preparing the Bank Reconciliation Statement it

will have to be added. Thus, you will find that when you prepare a Bank Reconciliation

Statement with an overdraft as per cash book as the starting point you will have to add all

items which were subtracted when you started with a favourable balance as per cash book,

and'vice-versa. This makes the preparation of the Bank Reconciliation quite complicated.

Hence, you are advised to follow plus and minus method. In that case by simply showing the

overdraft in the minus coluinn you will automatically have the desired effect of each item

duly adjusted in the overdraft. Look at Illustration 6. It starts with an overdraft as per cash

book. The overdraft is shown in the minus column of the Bank Reconciliation Statement but

all other item have been treated in the same way as in Illustration 5

Illustration 6

From the following p&ticulqrs ascertain the klallce as would appear in the bank pass book

of Ram Prasad on January 31, 1988. The cash hook showcd a credit balance of Rs. 8,200.

In Illustration 6, the starting point was the overdraft as per cash book. Let us see how a

Bank Reconciliation Statement is prepared if the starting point is overdraft as per pass book.

Look at Illustration 7 and compare it with Illustration 5. You will find that the treatment of

all items is the same. The difference lies only in showing the pass book balance. Since it is

an overdraft, it has been shown in the minus column.

Illustration 7

From the following particulars, ascertain the bank balance as it would appear in cash book

of Rati Ram on December 31,1987. His Pass Book showed an overdraft of Rs. 7,500.

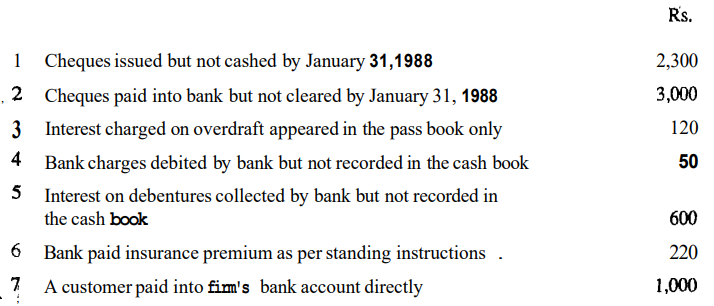

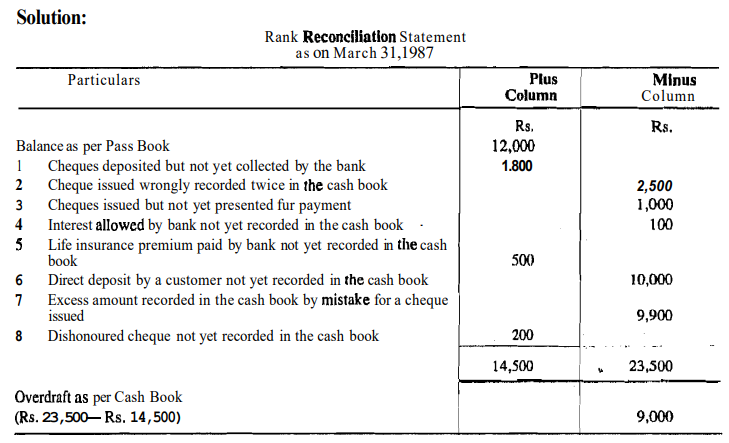

Illustration 8

Illustration 8

The pass book of Roshan showed a credit balance of Rs. 12,000 on March 31, 1987, while the bank column of his cash book showed an'overdraft of Rs. 9,000. Starting with the pass

book balance, prepare the Bank Reconciliation Statement using the following mformation.

1 - Of the cheques amounting to Rs. 8,000 deposited in the bank up to March 31, 1987, a

cheque of Rs. 1,800 was collected by the bank on April 3,1987.

2 - Cheque of Rs. 2,500 issued to Harish was wrongly entered twice in the cash book.

3 - Cheques issued during the month amounted to Rs. 8,000 of which cheques for Rs. 1,000

were not resented to the bank up to March 31, 1987

4 - The pass book showed a credit of Rs. 100 as interest for which there was no entry in the

cash book.

5 - The pass book showed a payment of Rs. 500 as life insurance premium for which no

entry was made in the cash book.

6 - The pass book showed a direct deposit of Rs. 10,000 from Mahesh on March 28, 1987.

It was entered in the cash book only on April 2, 1987.

7 - A cheque for Rs. 3,100 issued to a creditor was entered in the bank column of the cash

book as Rs. 13,000.

8 - The bank debited Roshan's account with a cheque for Rs. 200 received from Ajay

which had been returned dishonoured. No entry for dishonour was passed in the cash

book.

Note: In this illustration you find that the total of the minus column exceeds the totnl of tlie plus column. Hence

the difference of Rs. 9,000 is treated as overdraft as per cash book.

3.4.5 Adjusting the Cash Book Balance

When you look at the various items that nonnally cause the difference between the cash

book balance and the pass book balance, you will find a nuniber of items which appear only

in the pass book. Why not record such items in the cash book before preparing the Bank

Reconciliation Statement? This shall reduce the number of items responsible for the

difference. So, as soon as the pass book is received, the firm may record all those items in

the cash book which appear only in pass book and work out a fresh balance of the cash

book. This is called 'adjusted balance' or 'corrected balance' as per cash book. Similarly, it

may also pass correcting entries for tlie errors committed in the cash book and adjust the

cash book balance.

When you work out an adjusted balance of the cash book as above, the Bank Reconciliatior!

Statement may be prepared with this adjusted balance, This would reduce the number of

items shown in the Bank Reconciliation Statement. As a matter of fact, this is exactly what

is done in practice.

The items which can usually be adjusted in the cash book are :

1 Interest allowed by bank

2 Amounts collected by bank as per standing instructions

3 Payments made by bank as per standing instructions

4 Bank charges

5 Interest on overdraft

6 Direct deposits by customers

7 Dishonoured cheques or bills receivable

8 Errors committed in the cash book

Look at thc lllustration 4 again. You will find that out or^ tlle seven items causing the

difference four items can be adjusted in the cash book as follows :

The adjusted balance as per cash book is Rs. 8,060. Now, if we prepare the Bank Reconciliation Statement wjth the adjusted balance, it will appear as follows :

Thus, you observe that the Bank Reconciliation Statement prepared with the adjusted balance included only three items. These items could not be adjusted in the cash book because they had already been recorded in the cash book correctly. The difference arose only on account of the time lag.

It may however be emphasised that you should concentrate on preparing the Bank .

Reconciliation in the normal manner. The statement with an adjusted balance of the cash

book is to be prepared only when it is specifically asked far.

3.4.6 Advantages of Bank Reconciliation Statement

The main purpose of preparing Bank Reconciliation Statement is to account for the

difference between the cash book and the pass book balances. This would ensure the

accuracy of entries made in the cash book as well as those in the pass book. Regular

. comparison of these two books is necessary for preparing the Bank Reconciliation

Statement. This helps in the detection of errors and taking timely action to correct them. It is

quite possible that the bank wrongly debits firm's account for cheques drawn by someone

else. If reconciliatibn is not done, such mistakes will not be detected. Preparation of Bank

Reconciliation Statement also helps in preventing frauds in banking transactions. The

cashier, for example, may omit to deposit some bearer cheques in the bank and encash them

himself. Such fraud is sure to be detected at the time of reconciliation when it is

investigated as to why certain cheques remained uncollected. Thus, it acts as a moral check

on the staff to refrain from indulging in such activities.

Bank Reconciliation Statement is alsorequired for audit purposes. The auditor has to verify

the bank balance before he would certify. the accounts. For this he would insist on the Bank

Reconciliation Statement and ensure that the bank balance shown in the cash book is

correct.